This article discusses the primary difference between undistributed budget and management reserve as well as their intended proper uses. This explanation reflects the accepted standard since the advent of the concept known today as EVMS.

Undistributed Budget

Undistributed budget (UB) is the budget and its associated statement of work (SOW) for work not yet authorized to a control account manager (CAM) or managers. A common misconception is that UB is budget and work effort set aside because the details are uncertain. The opposite is true. Undistributed budget must always have a specific SOW for the budget amount identified in the UB log. Because UB must have SOW associated with it, it is not management reserve (MR).

Undistributed budget provides the mechanism for a contractor to:

- Set aside the SOW and budget for a portion of authorized unpriced work (AUW) to undertake newly authorized contract work quickly. This allows a contractor to proceed with time phasing the SOW and budget immediately after receiving an authorization to proceed (ATP) for work not yet negotiated (or not yet definitized which is the same as authorized unpriced work). The contractor is expected to distribute a portion of the AUW’s SOW and budget for the near term control account tasks, leaving the balance of the SOW and budget in UB. This is done to avoid having to take back budget from the CAMs in the event of negotiation loss. Remember that budget and SOW must always be authorized or de-scoped together. If a company begins to take back budget from CAMs without the associated SOW to balance the UB log for a negotiation loss, the CAMs begin to distrust the process resulting in a serious undermining of the EVMS processes. After negotiations are complete, the negotiation loss is debited from the UB, noted in the UB log, and the balance of the SOW and budget distributed to the CAMs. This should typically occur within two accounting periods after negotiations are completed.

- Process a customer stop work order (SWO). Anytime the customer issues a SWO to a contractor, the value of the budgeted cost of work remaining (BCWR) and its associated SOW is removed from the respective CAMs involved (and the performance measurement baseline or PMB) and credited in the UB log until the customer redirects the contractor. The BCWR is the difference between the CAM’s budget at complete (BAC) and cumulative performance (BCWP) to date or BCWR = BAC – BCWP cum.

- Process an internal work transfer or stop work order (SWO). The UB log becomes the transaction record for traceability. This logging is necessary for possible new make/buy decisions, CAM to CAM transfers, as well as for internal SWOs. Note this is not done in the management reserve log as MR never has SOW identified.

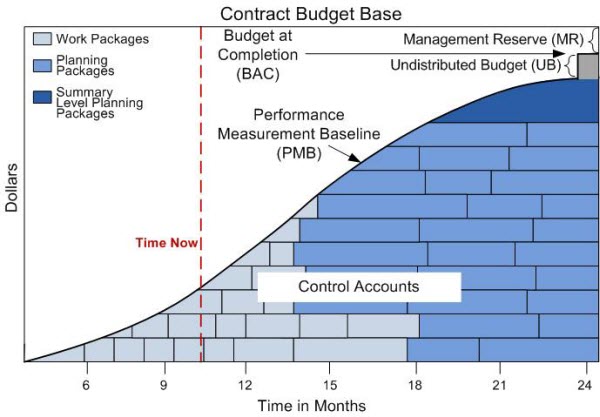

Additionally, once budget is distributed, it is assigned to a control account and time phased (BCWS) to reflect the scheduled work. Remember that the distributed budget reflects a signed, CAM level work authorization document (WAD) with a detailed SOW, budget (by cost element), and a period of performance (the schedule). The work scheduled in the near term, typically the next six months, must be detailed in work packages. Work scheduled in the future months is time phased in planning packages (not yet detailed). In some instances, future work SOW and budget may be assigned to a summary level planning package (SLPP), typically a WBS level element, prior to being assigned to one or more control accounts. In this instance, work not yet detailed is part of the summary level planning package or control account planning packages, not undistributed budget.

One more point about UB. It is not time phased. It is a part of the performance measurement baseline (PMB), but is added to the end of the PMB curve to equal the total project BAC.

This discussion on time phasing the performance measurement baseline (the distributed budget) using a rolling wave planning process and the relationship to undistributed budget is illustrated below.

Management Reserve

In the EVMS vernacular, management reserve (MR) is the budget set aside for Known Unknowns – not Unknown Unknowns. This distinction is important, as the budget at complete (BAC) plus MR equals the contract budget base (CBB).

Management reserve is typically used when an identified risk is realized (Known Unknowns). Once a risk has become a reality, such as re-work, re-test, re-make, more lines of software required, etc., the newly identified work required to satisfy the existing contract SOW must be scheduled and resource loaded (BCWS). This additional budget must be distributed to a CAM (or CAMs) via a work authorization document. The source for this budget is MR and not UB, as UB must have previously been logged with a predetermined budget and associated SOW.

While the Unknown Unknowns could be estimated using simulations, models, etc., the project does not have the luxury to have such a budget set aside initially for an Unknown Unknown occurrence. If an Unknown Unknown becomes a Known, thus the newly identified risk has become reality, the contractor could use the existing MR to budget this newly identified task or tasks to satisfy the contract requirement.

When there is no MR, the contractor must incorporate an over target baseline (OTB) in the event newly identified risks are realized. Most projects at this juncture invoke an OTB, as there usually is insufficient MR remaining. During recent years there have been instances when an Unknown Unknown occurred on DOE, NASA, and DOD programs. A tornado took out the reactor on the DOE Clinch River Breeder Reactor program before completion. The Northridge earthquake disrupted building occupancy and took out freeway overpasses, seriously impacting the NASA Space Station program and the F-22 and F-35 programs. Sometimes the contractor can successfully renegotiate the remaining work under the force majeure clause. Since budget is strictly a metric and is not funds, a realistic and detailed estimate to complete (ETC) and estimate at completion (EAC) must always be forthcoming. However, the source for the budget for the newly identified work must come from MR.

Because the equation BAC + MR = CBB must be honored, there is scant chance that a contractor will negotiate a cost plus or fixed price contract (not firm fixed price) with a contract target cost (CTC) where there would be a management reserve budget sufficient to handle the Unknown Unknowns, nor should there be at the onset of a project.

Contractors awarded cost plus or fixed price type contracts in the U.S. can at best set aside five to ten percent of the negotiated contract value (the contract target cost, or CTC), for MR. This small amount would be considered petty cash with respect to the Unknown Unknowns. Consequently, this insufficient amount for the Unknown Unknowns risk materialization is the primary reason why over target baselines (OTBs) are eventually implemented on most risky projects.

|

|

Download this Article as a PDF |