Revision September 20, 2023

This article discusses the issues that commonly surface with authorized unpriced work (AUW) or undefinitized contract actions (UCAs). In some instances, contractors are not following the commonly used and recommended practices. This discussion applies to all government agencies, so while this article will identify terms that apply to DoD and NASA, it will also include terms common to DOE, such as project budget base (PBB).

Background

To set the stage for this discussion, it is useful to review a few EVM concepts.

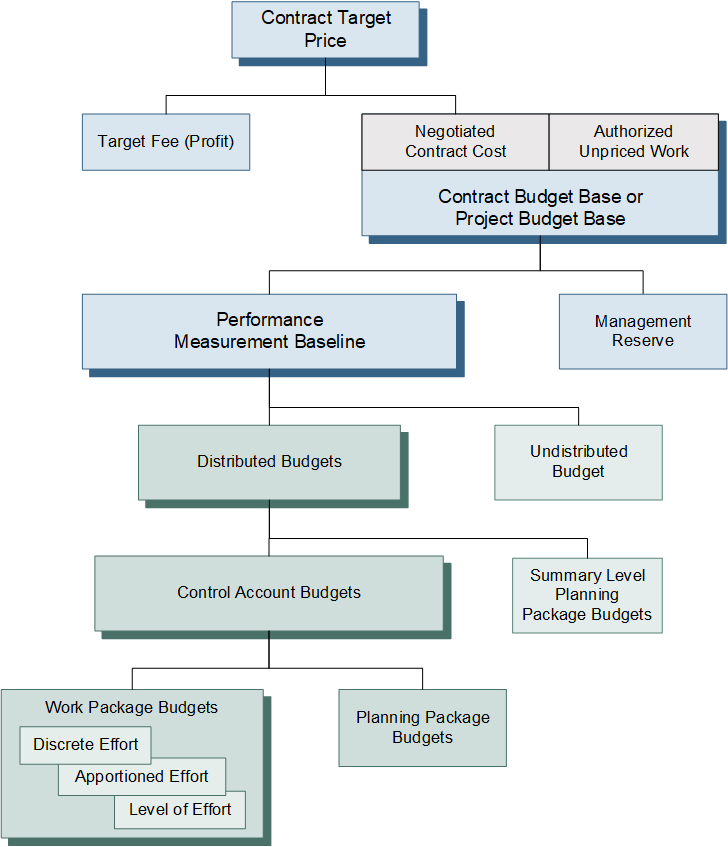

The contract budget base (CBB)/project budget base (PBB) represents the base cost of contractually authorized work, including changes, from which the performance measurement baseline (PMB) is developed to measure future performance. The CBB/PBB (and subsequently the PMB) excludes any fee or profit. When all authorized work has been negotiated, the CBB/PBB equals the negotiated contract cost (NCC). When there is AUW/UCA work involved, the CBB/PBB includes the contractor’s estimate to accomplish the work. The NCC is not changed until the effort is negotiated. Figure 1 illustrates the budget distribution flow down process.

Figure 1 – Budget Distribution Flow Down

It is also useful to know the requirements for handling authorized unpriced work are addressed in numerous industry and government agency documents including the:

- EIA-748 Standard for EVMS guidelines.

- NDIA IPMD EIA-748-D Intent Guide (August 2018).

- DoD Earned Value Management Implementation Guide (EVMIG) (January 18, 2019).

- DoD Earned Value Management System Interpretation Guide (March 14, 2019).

- DOE Office of Project Management (PM) EVMS Compliance Review Standard Operating Procedure (ECRSOP) Appendix A Compliance Assessment Governance (CAG) 2.0 (June 1, 2022).

The following table of the applicable EIA-748 guidelines provides a list of related industry or government references you can review that discuss AUW.

|

EIA-748 Guideline Reference |

Industry or Government References |

|---|---|

|

Guideline 8 – Establish the Performance Measurement Baseline “Initial budgets established for performance measurement will be based on either internal management goals or the external customer negotiated target cost including estimates for authorized but undefinitized work. Budget for far-term efforts may be held in higher level accounts until an appropriate time for allocation at the control account level.” |

NDIA IPMD Intent Guide, Guideline 8 DoD EVMSIG, Guideline 8 DOE CAG, Subprocess C. Budgeting and Work Authorization, C.1 Scope, Schedule, and Budget Alignment |

|

Guideline 14 – Identify Management Reserve and Undistributed Budget |

DoD EVMSIG, Guideline 14 DOE CAG, Subprocess C. Budgeting and Work Authorization, C.11 Undistributed Budget (UB) Both state that scope and associated budget that may reside in UB includes AUW. |

|

Guideline 15 – Reconcile to Target Costs |

DoD EVMSIG, Guideline 15 DOE CAG, Subprocess C. Budgeting and Work Authorization, C.12 Reconcile to Target Cost Goal |

|

Guideline 28 – Incorporate Changes in a Timely Manner “Incorporate authorized changes in a timely manner, recording the effects of such changes in budgets and schedules. In the directed effort prior to negotiation of a change, base such revisions on the amount estimated and budgeted to the program organizations.” |

NDIA IPMD Intent Guide, Guideline 28 DoD EVMIG, 2.5.2.2.1 Authorized Unpriced Work (AUW) DoD EVMSIG, Guideline 28 DOE CAG, Subprocess G. Change Control, G.2 Incorporate Changes in a Timely Manner, Effectiveness Criteria G.2.3 |

Applying the EIA-748 Guidelines for AUW in an EVM System Description

The documents referenced above all state that contractors are to budget for the AUW they receive from the customer by using their estimates for what it will take (the resources) to do the work. Items related to Guideline 28 discuss the post negotiation actions when the contractor must adjust the originally identified budgets down to the negotiated value of the contract change.

The above references from the EIA-748, industry guidance, and government implementation and interpretation guidance clearly demonstrate the basis for handling authorized unpriced work is through undistributed budget. In practice this means:

- Authorized unpriced work budget typically resides in undistributed budget (UB), with budget being incrementally issued to control accounts for near term work until the change is eventually negotiated (hopefully, within a relatively short period of time).

- Summary level planning packages (SLPPs, or other similar names) can also be used when the contractor’s EVM System Description allows for them. SLPPs are mechanisms encouraged by the EIA-748 Guidelines and government implementation/interpretation guidance that allow a contractor to move the budget from undistributed budget into the distributed budget at a higher level than the control account. This mechanism enables the contractor to distribute budget from UB in a timely manner (even though they should not have to for AUW), and it allows contractors to retain their flexibility in determining any management reserve (MR) following negotiation of the AUW.

- In those cases when negotiations take longer than expected, contractors sometimes end up distributing the entire budget from UB to control accounts electing not to hold back MR budget thinking the customer will automatically take that budget back as “not needed” during negotiations, even though government language is clear that is not to happen.

-

Once the AUW change is negotiated, the contractor then has to make the necessary adjustments to the budgets for the yet-to-be-distributed work residing in UB. This is also when a contractor determines an MR amount to withhold and distributes the remaining scope and budget to control accounts.

- In those instances when negotiations take a long time, and all the budget has been distributed to control accounts, the contractor may have to adjust (reduce) control account budgets to accommodate the negotiation losses. This may include identifying MR budget.

- Some contractors elect to use existing MR (if any exists) to compensate for negotiation losses instead of taking back budget from the control accounts. This is at the Project Manager’s discretion, it is NOT required. The customer cannot require the contractor to use MR from existing scope of work to cover new work (AUW) or to adjust budgets once AUW is negotiated.

- If a contractor had used SLPPs, they could have used these accounts to make the final distributions to control accounts and to MR, instead of having to take budget back from control accounts.

Some customers in the past have incorrectly told contractors how to incorporate AUW changes. A typical request was to tell a contractor to use their existing MR to do so. This is incorrect since MR is intended for possible use on the existing contract scope of work, not for any new contract scope. Guideline 28 makes it clear that UB is the correct place for these AUW activities to be transacted.

Some customers have also convinced contractors that they should only plan and budget to the not to exceed (NTE) that might be attached to an authorization to proceed (ATP) with authorized unpriced work. An NTE is typically a billing or spending limitation placed on AUW and should not be confused with the total amount the contractor believes the undefinitized work will eventually cost. When there is a question about the proper approach, then contracting officers should clarify that NTEs should NOT impact the PMB or CBB/PBB amounts.

For unpriced change orders, the contractor will need to develop its best estimate for planning and budgeting purposes for incorporation into the PMB.

Under a “spending” NTE, the contractor is to report to the customer when their expenditures are nearing the NTE spending limitation, so the customer can either arrange to get additional funding and increase the NTE value or instruct the contractor to slow down or stop working along their PMB planned for that work (usually resulting in a customer-driven impact to the schedule and cost forecast for that work).

In some cases, the customer comes into an AUW situation with a specific dollar value in mind about what the total cost for a particular change should be, calling this the “NTE.” If the contractor and the customer previously agreed that the change would not be higher than a certain amount, then this would probably be acceptable. If it is a unilaterally determined amount by the customer, and the customer does not allow a bid to be higher than the “NTE” amount, it can result in unrealistic project budgets when the contractor is forced to perform to an inadequately priced program.

NOTE: Unfortunately, as currently written, the EVMIG (January 18, 2019) and the EVMSIG (March 14, 2019) contradict one another. EVMIG Paragraph 2.5.2.2.1 in part states:

“The written authorization defines the scope of work that needs to be accomplished and may include a Not-To-Exceed value.”

As written, this could be misleading. As pointed out in the paragraph immediately above, using an NTE is only allowed if both parties mutually agree that the change would not be higher than a specified dollar value (i.e., may be acceptable to have an NTE so long as the entire cost estimate is planned out for the AUW).

The EVMSIG discusses the AUW process more completely.

|

|

Download the Handling Authorized Unpriced Work in an Earned Value Management System PDF Article |